Risk Commentary

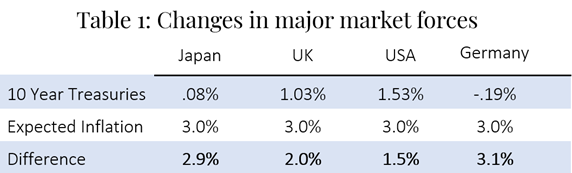

TINA is an abbreviation of “There is No Alternative”, meaning that despite the distortions caused by the Quantitative Easing (QE) of central banks, institutional investors are basically forced to bend their investment guidelines in an attempt to achieve reasonable returns. Hence, the pushing of many investors out on the risk spectrum and a rise in valuations for most financial assets. Many would argue that support for asset values is exactly the point of QE and that the programs have been successful beyond what many central bankers had ever imagined. Basically, government demand has replaced an absence of private sector demand and with the supported asset prices, the normal market forces will truncate the deleterious effects of the 2008 Credit Crisis and now, the COVID crisis. However, is it really that easy? Can we assume that the private sector will re-establish normal operations and central banks can resume their normal roles? Our view is that like many quick fixes, it is easy in the initial phase but the extraction is very difficult. For example, based on inflationary expectations of approximately 3%, 10 year Treasuries should yield approximately just that, 3.0%. With yields near 1.5%, we are approximately 150 basis points shy. However, in Europe and Japan, the situation is more dire with the shortfall being 200 basis points or more:

So you might ask, ”Where is the problem? “We have adjusted and are now living with TINA.” Well, the problem comes with the exit process. Just like the person who jumped from the 50 story building might conclude there is no problem when reaching the 40th or 30th floor, the pain has yet to come. So the problem is: can the central banks exit their QE process in a graceful manner? Our view is that the central banks are ultimately controlled by politicians, and those politicians want to be re-elected, which translates into low interest rates and a robust economy. Hence, the pressure on central banks to not exit is enormous. In fact, the contentiousness with re-electing Powell to the FED is focused on the extent to which he has supported programs which aid average workers, which ultimately translated into lower interest rates and a continuation of QE.

So where does all this lead? Can there be a continuation of QE with few repercussions? Our view is that the adage of “No Free Lunch” remains operative. Retirees are realizing the money they set aside will not provide the lifestyle they expected and the institutions which had relied on asset earnings to cover future liabilities are likely to be pressed, at least in the short-run. What about the massive debt build-up as a result of governments enhancing social programs? All reasonable concerns which hopefully will be addressed in future installments.

China: A Sea Change

Why has the central government in China allowed a major firm such as EverGrande to default, effectively taken control of Alibaba, delayed the delivery of various goods, and outlawed energy-sapping crypto currencies? It is possible that these measures are simply efforts of the central government to improve the overall running of the country. However, it could be something much larger which might impact all of us. Assuming that the central government has control of most aspects of the economy, it might suggest that the central government is making every effort to garner financial resources. The COVID-19 crisis has touched every country including China. However, in contrast to many other developed economies, China is dependent on the generation of foreign currency reserves via numerous manufacturing operations which historically have operated on thin margins and dependent on high volumes. With the volumes down and the margins still slim, cashflow might be pressed, particularly in the absence of large public offerings (which were curtailed by the SEC) and the shift in Hong Kong’s status in the financial markets. While the nationalist might cheer the possible weakness of a financial rival, some discretion is probably in order. Germany progressed from being essentially bankrupt during the Weimer Republic years to control of continental Europe a mere 10 years later. Likewise, China has massive resources at its disposal.

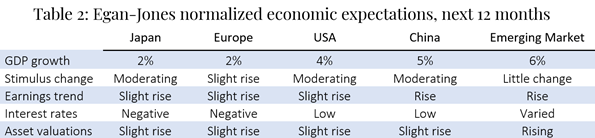

Below is a summary of our expectations for the various economies:

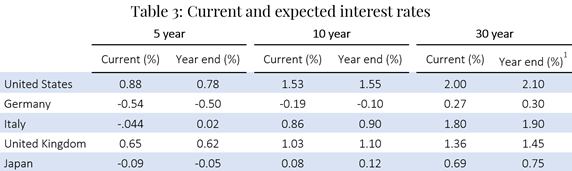

Regarding trends, we had expected a slight decline in the 5 year rates with the passage of the US budget crisis and a rise in longer rates to reflect inflation concerns:

Source: https://tradingeconomics.com/bonds, https://www.bloomberg.com/markets/rates-bonds/government-bonds/us, http://www.worldgovernmentbonds.com/country/italy

Source: https://tradingeconomics.com/bonds, https://www.bloomberg.com/markets/rates-bonds/government-bonds/us, http://www.worldgovernmentbonds.com/country/italy

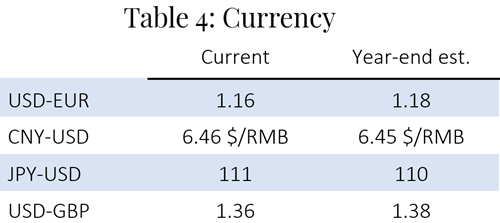

Below are our expectations for major currencies:

Source: https://www.x-rates.com/table/?from=USD&amount=1

Source: https://www.x-rates.com/table/?from=USD&amount=1

How we can help

Prospective clients have often asked how we can help them and what areas we consider are particularly

strong. In response, below are the areas worth reviewing:

Private Placement Ratings – assisting investors access private markets via ratings on private placements.

Subscription Ratings – we have had a strong track record in providing early, accurate independent credit

rating research.

Climate Change / ESG Scores – an assessment of entities’ current and prospective scores.

Independent Proxy Research and Recommendation/Voting – assisting fiduciaries in fulfilling their voting and record-keeping obligations.