Risk Commentary

Taking Measure of the Major Risks, Probabilities and Possible Impact

It is incumbent upon risk managers to be knowledgeable of the major risk factors, the drivers of those risks, the likely outcomes, and probabilities. We review these factors on a semi-annual basis to provide at a high level, some of the challenges and possible impact. While alarmist headlines gather significant attention and the research area is well-populated with alarmists, our bent is to provide a measured view in an aim to be most helpful to our readers.

While there is little doubt that the risks and challenges are many, our view is that a melt-down is extremely unlikely given the markets’ tendency to self-correct and the enhanced power of the central banks. A major private debt investor mentioned last week that their business was up over 50% year to date and that they viewed the current environment as akin to a “Goldilocks” environment; despite the negative headlines, structures and equity cushions had improved, portfolio company results were strong, and because of the increase in interest rates, yields were improved.

In this installment we address political issues because of their impact on the markets and related risks but aim to do so from an apolitical perspective.

Dysfunctional Policies

The approval rating of the current administration is a recent low arguably because policies have proven to be painful for the average voter. Our view is that voters typically (the major exception being times of war or civil strife) make an assessment based on their own narrow interests and the combination of inflation, increased interest rates, and embarrassments in Afghanistan have pressured the approval ratings.

Many of the policies of the current administration can be traced to efforts in addressing demands of Democratic party factions which are at odds with fighting inflation. For example, drilling for energy has been discouraged while President Biden is going hat in hand to Saudi Arabia and Venezuela in an attempt to encourage additional energy production.

While it is easy to criticize the current administration, the most vibrant segment of the Democratic Party has been the Progressives and there was a real risk of fracturing (in a manner that Ross Perot did in 1992). Nonetheless, House majority might slip (or change) and perhaps as a result some of the Progressives’ demands will moderate.

Inflation/Rising Interest Rates

Many were surprised by the rapid rise in inflation and assumed it would ease in months (the term used was “Transitory”). Many believe the root cause was monetary expansion; that is, the supply of money exceeded the growth of the economy. While much of that is true, another component is the nature of the spending; the increased spending was not for an enhancement of productivity, but rather the additional spending was for COVID-related income maintenance, and Ukraine War spending. While the COVID expenditures have eased, the Ukraine War spending continues.

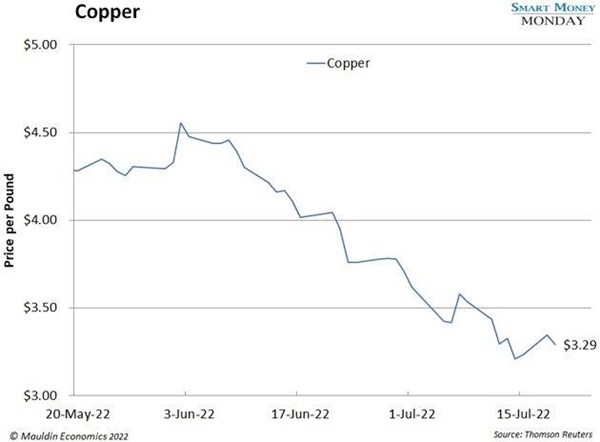

Some of the inflationary pressures are abating per the below charts on gasoline and copper prices from Trading Economics.

Figure I: Gasoline (USD/Gal)

Figure II: Copper (USD/lb)

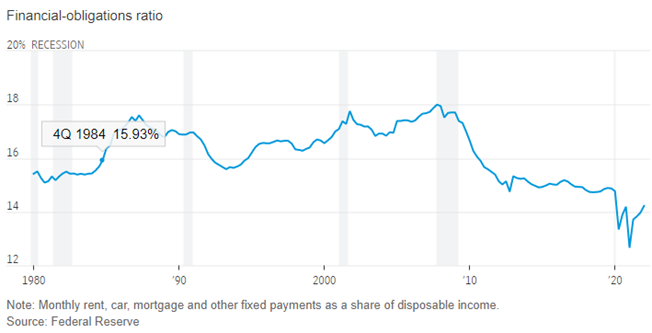

Figure III: Financial Obligations Ratio

Furthermore, from a consumer perspective, the Financial Obligations ratio is fairly modest.

Ukraine War

In the above section we mention the effect of the war on fiscal policy, but the risks are more extensive. As is often the case with wars, they continue and escalate until one side exhausts its and its allies’ resources. That path appears to be the case here whereby every month, the U.S. announces the delivery of evermore sophisticated and extensive weapons systems. As of several months ago, there was the understanding that the U.S would not provide fixed wing aircraft to Ukraine, but that now appears to be breached.

Just to be clear, the under-lying premise of Russia’s actions was apparently the closing of access points to Russia and control of some of the few natural gas sources in Europe. As can be seen below, natural gas prices in Germany are severely elevated:

Figure IV: Germany THE Natural Gas Forward Month 1 - Mid Price (EUR/MWh)

Meanwhile, for the U.S., the premise appears to be to weaken Russia such that it is less of a threat to NATO countries. By the way, China appears to be employing the U.S’s apparent strategy against the U.S., that is, where possible take actions to weaken the U.S.

Many are concerned that we are fighting the last war, (i.e., the Cold War with Russia) and that despite the bluster, Russia is a manageable threat. Particularly irksome is that the countries which are most threatened by Russia’s actions (i.e., Germany and France) are hamstrung by their dependence on Russian energy, and on a relative basis, are providing minimal support.

Presidential Politics

Although the Presidential elections are more than two years away, preparations are being made currently, and that has us worried. On the one hand, the current administration’s approval rating is low and numerous sources are questioning the age and fitness of Mr. Biden’s running for a second term. The normal process would be the grooming of possible successors by providing a platform and spotlight for preferred candidates. That is not happening as Mr. Biden is insisting on running for another term (prior campaign promises notwithstanding). On the other hand, Mr. Trump is crisscrossing the country with campaign rallies while the Jan. 6th commission is threatening criminal charges connected with his role in the event. Many are suggesting candidates such as Florida’s Ron DeSantis as having broader appeal, but Mr. Trump might be hard to deny given his resources and network. Furthermore, Mr. Trump might feel inclined to run given that the Democrat’s control of the House is likely to diminish or pass to the Republicans and Trump might feel compelled to vindicate himself.

Many market observers might prefer a new slate of candidates (such as Pritzker and Newsom on the Democratic side and DeSantis and Pence on the Republican side) but, with the exception of Obama, few are vaulted to the forefront without the support of the incumbents.

Market Decline

The decline in the equity markets has many worried that we are entering a recessionary period.

The fact that long-term rates are below short-term rates could indicate that market participants believe a recession is pending. Alternatively, the inversion could indicate that inflation is likely to ease and that rates will normalize.

China

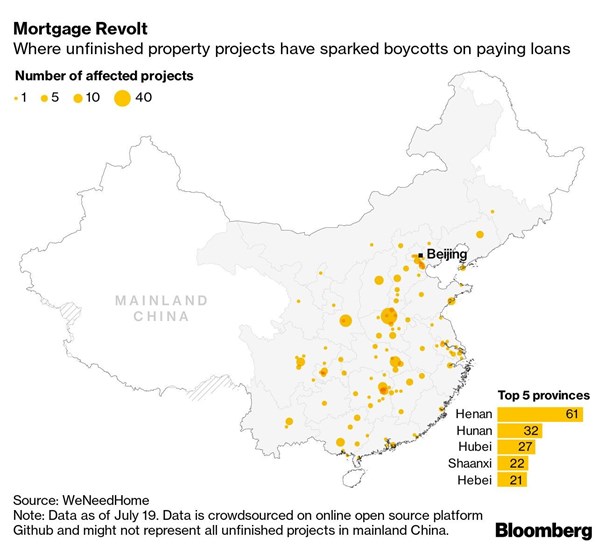

From an economic perspective, there is little doubt that China has made massive strides over the past several decades. The leadership’s belligerence might be masking underlying concerns. The COVID lockdowns have hurt many, but perhaps the larger issue is an apparent loss in faith in the attractiveness of the housing market. The failure of several large developers and the refusal of people to make mortgage payments on second homes has the potential for widespread breakdowns.

Figure V: Property Projects Affected by Boycott

Residential housing market downturns are painful and have caused more than one recession including the late 1980s/early 1990s S&L crisis, and the 2008 Credit Crisis (because of the widespread impact).

How we can help

Egan-Jones Ratings Company started providing ratings in 1995 for the purpose of issuing timely, accurate ratings. EJR is a Nationally Recognized Statistical Rating Organization (NRSRO) and is recognized by the National Association of Insurance Commissioners (NAIC) as a Credit Rating Provider. EJR is certified by the European Securities and Markets Authority (ESMA) and recognized as market leader in Private Placement ratings. EJR also provides independent credit rating research, Climate Change / ESG scores, and Proxy research and recommendations.

Prospective clients have often asked how we can help them and what areas we consider are particularly

strong. In response, below are the areas worth reviewing:

Private Placement Ratings – assisting investors access private markets via ratings on private placements.

Subscription Ratings – we have had a strong track record in providing early, accurate independent credit

rating research.

Climate Change / ESG Scores – an assessment of entities’ current and prospective scores.

Independent Proxy Research and Recommendation/Voting – assisting fiduciaries in fulfilling their voting and record-keeping obligations.

Egan-Jones rates a wide variety of private placements:

Aircraft Lease and Loans

Airline Lease Back

Asset-backed loans

Bank, BDCs

Credit Facility/ Warehouses

Corporates

Credit-Tenant Loans (CTLs)

Equipment Leases

Financial Institutions

Ground Leases

Insurance

Middle Market Lending

Project Finance

Real Estate, REITs

Specialty Finance

CRE Loans, Other

Funds:

Closed-end Funds

Credit Funds

CRE Funds

Direct Lending Funds

Feeder Funds

Infrastructure Funds

Liquidity Funds

Mezzanine Funds

Mixed Strategy Funds

Opportunistic Funds

Real Estate Funds

Structured Debt Funds

Click here to view sample Private Placement transactions.