Risk Commentary

The market is on the verge of a major inflection point; the uncertainty is which way is it heading. Over the past few weeks, the equity market has been fairly volatile despite no real change in the macro fundamental outlook. The U.S. Fed has remained dovish, and the US stimulus was released as planned. European COVID-19 situation is lagging behind that of the US and UK. After a year of global effort, the major economies are on the verge of becoming inoculated from the dreaded COVID19 disease. Unprecedented is probably the best way to describe the massive undertaking of drug discovery and rollout. Hence, after a year of lockdown, it appears consumers are anxious for a return to normal and make up for some delayed spending. Now for the concerning issues. A massive rise in social spending combined with tax increases has many worried that the recovery will be stalled by nonproductive spending. Providing support for this notion is the recent rise in interest rates, although some would argue the rise was driven by the expected increase in spending. The big issue facing most investors is whether inflation is going to kick-up and result in massive disruption in portfolio positions.

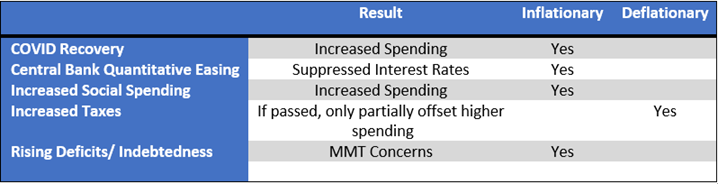

While it is difficult to assess the future, it is worthwhile to note some of the major forces shaping the markets over the next couple of quarters, and most importantly, possible outcomes:

There are signs the market is struggling with the new conditions such as tighter cover rates in recent Treasury auctions and the rise in some of the crypto currencies. Assuming we have properly identified some of the major forces driving the market over the next couple of quarters, it appears the forces leading to increased inflationary pressure outweigh those on the deflationary side. Hence, perhaps the recent rise in interest rates is here to stay. In Europe, the major differences have been and continue to be a lower overall rate of growth and lower, and in many cases, negative interest rates. A major assumption in the above chart is whether the current administration is going to continue its approach; our view is that despite the protestations of the Republicans, the current administration is likely to be remembered as one of the most progressive since FDR and will succeed in advancing a variety of pro-spending legislation. For those Milton Friedman followers, the expansion in currency beyond the growth in the economy, normally results in inflation. The QE of the central banks has delayed but perhaps not completely eliminated inflationary pressures. In retrospect, the first few quarters of 2021 might be remembered as a major inflection point in the economy.

How we can help

Prospective clients have often asked how we can help them and what areas we consider are particularly

strong. In response, below are the areas worth reviewing:

Private Placement Ratings – assisting investors access private markets via ratings on private placements.

Subscription Ratings – we have had a strong track record in providing early, accurate independent credit

rating research.

Climate Change / ESG Scores – an assessment of entities’ current and prospective scores.

Independent Proxy Research and Recommendation/Voting – assisting fiduciaries in fulfilling their voting and record-keeping obligations.