Risk Commentary

China Challenges; Inflation Imbroglio; France being French (Apr 2023)

Countries, like companies, must adapt their behavior to address challenges. From the mid-1930’s to 1940’s, the U.S. supported the Republic of China to counter Japan's expansionary efforts. However, the Chinese Communist Revolution led to a new government and the establishment of the People’s Republic of China in 1949. Once an ally, the country of China became an enemy in the Korean War (de facto 1950 – 1953) upon General MacArthur’s advancing well past the 38th parallel (the demarcation between North and South Korea).

Rolling forward to Nixon's presidency, China's opening led to a reduction in most manufacturing costs and significant economic growth for China. However, in recent years, the U.S. and other nations have started to view China as a strategic threat, taking measures to limit Chinese imports, restrict the use of telecom technology from companies like Huawei, and limit access to Western technology.

Taiwan's sovereignty remains a contentious issue, but with the ongoing situation in Ukraine, it seems that cooler heads may prevail, recognizing the challenges of executing and supporting an amphibious landing 90 miles away. Opinions on China's future vary widely, with some like Ray Dalio (Bridgewater founder) believing that China is on the rise as the U.S. declines. On the other hand, geopolitical analyst Peter Zeihan argues that China's population growth collapse and dependence on long supply lines for energy make it highly vulnerable.

France has finalized its inaugural yuan-denominated liquefied natural gas (LNG) transaction, procuring 65,000 tons of LNG from the UAE. The deal took place on the Shanghai Petroleum and Natural Gas Exchange, emphasizing China's initiative to encourage the use of the yuan in international commerce and challenge the US dollar's supremacy, especially in the energy industry.

At present, the yuan's share in worldwide trade is a mere 2.7%, in contrast to the US dollar's 41% share [1]. The adoption of the Chinese currency has been gaining traction lately, as Russia has shifted towards yuan-based trading in response to Western sanctions on its exports, imports, and energy transactions.

This progress is also in line with a recent agreement between Brazil and China to forgo the US dollar in certain trade operations, opting to use their respective currencies instead. This further demonstrates China's efforts to establish the yuan as a more prominent currency in the global economy.

So where does that leave us? Our view is that China has and will continue to experience bumps, but over the longer term will determine that it is optimal to be a decent global citizen. We are rather optimistic and that over time, overall conditions continue to improve and that some sort of accommodation is reached.

Inflation Imbroglio

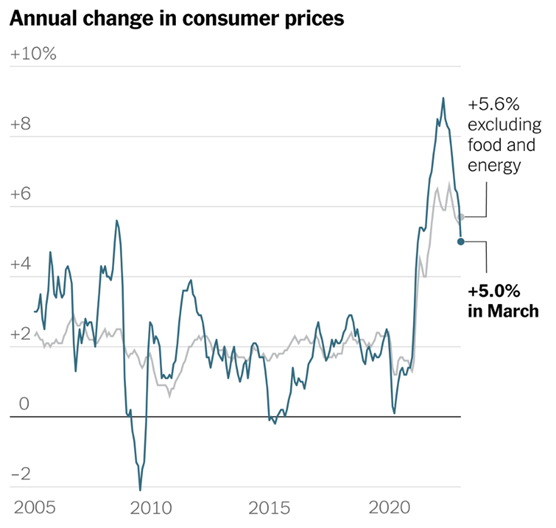

Figure I: Change in Consumer Prices (% per year)

The markets have been whipsawed by the rapid, massive rise in the Fed Funds rate, which changed 475 bps from March 17, 2022, to March 2, 2023 [1]. The impact has been especially severe on assets considered to be risk-free, which have experienced significant losses. Additionally, assets with moderate duration, like low-yielding mortgage assets, have gapped out due to homeowners' declining interest in acquiring higher-cost mortgage assets. As shown below, the real estate sector has seen massive shifts:

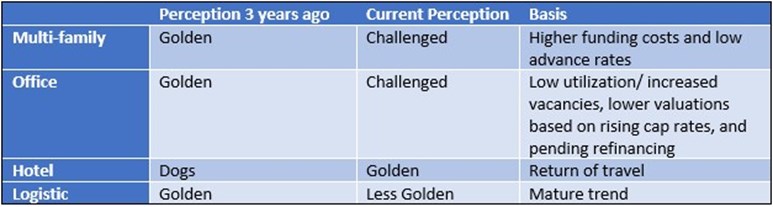

Figure II: Shift in Real Estate Sector

Banks hold many of these assets; determining the level of exposure is crucial. Losses on held-to-maturity assets can be determined relatively easily from public filings. The FDIC's latest report for the fourth quarter of 2023 shows that unrealized losses on held-to-maturity securities totaled $340.9 billion [3].

With total bank quarterly net income at $68.4 billion, these losses would be absorbed over approximately one year at the current rate if they had to be recognized immediately, which is typically not the case. Instead, the securities are likely to be held to maturity and redeemed at face value.

Meanwhile, interest rates may fall again, reducing unrealized losses, and the Fed is providing funding at face value for the securities for the next 11 months. (Note, a proper analysis should be done at the level of each institution rather than on a gross basis).

Regarding real estate exposures, commercial real estate, particularly high-profile, highly leveraged assets, raise concerns. Generally lower loan-to-value (LTV) ratios for second-tier properties provide a cushion against default and loss, despite a more significant percentage decline in annual operating income. While simplistic, the below example might be enlightening.

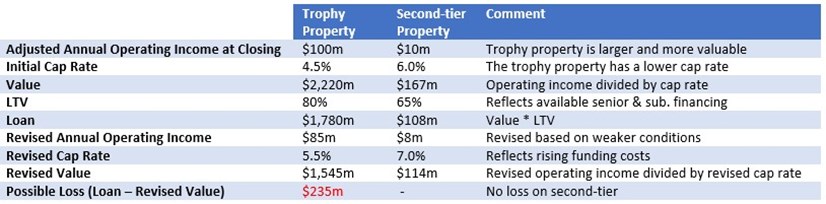

Figure III: Hypothetical Property Performance

As can be seen above, the lower advance rate (or LTV) for the second-tier property provides cushion such that despite a more drastic percentage decline in annual operating income, the loan is less than the value of the property, thereby theoretically reducing the probability of default and loss given default. Additionally, the second-tier property likely has more amortization than the trophy property, thereby providing additional “cushion’. In the above example, the break-even (i.e., no subsequent losses) initial LTV for Trophy Property is 69.5%. (Note, all information provided is hypothetical, but hopefully illustrative).

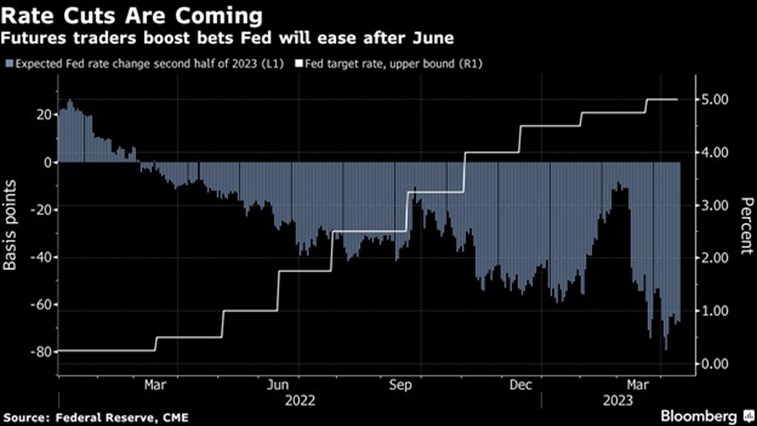

The below figure supports the expectations of future rate cuts.

Figure IV: Fed Funds Rates and Expectations

France being French

French President Emmanuel Macron visited China recently whereby Macron argued that the EU needed to "create the conditions for more strategic autonomy," including on China [4]. The statement caused a stir particularly in light of the substantial aid being provided for the defense of a European neighbor.

____________________________________________

[1]https://www.forbes.com/sites/miltonezrati/2023/01/26/yuan-pipe-dreams

[2] https://www.forbes.com/advisor/investing/fed-funds-rate-history/

[3] https://www.fdic.gov/news/press-releases/2023/pr23013.html

[4]https://www.aa.com.tr/en/politics/china-trip-by-frances-macron-eu-commission-chief-stirs-public-relations-disaster/2873368

How we can help

Founded in 1995, Egan-Jones is a Nationally Recognized Statistical Rating Organization (NRSRO) and is recognized by the NAIC and is certified by ESMA. We can help in the following areas:

Requested Ratings – we assist investors access private and public markets via ratings.

Subscription Ratings – we provide early, accurate, and independent credit rating research.

Independent Proxy Research and Recommendation/Voting – we assist fiduciaries fulfill their voting and record-keeping obligations.

Egan-Jones rates a wide variety of private placements:

Aircraft Lease and Loans

Airline Lease Back

Asset-backed loans

Bank, BDCs

Credit Facility/ Warehouses

Corporates

Credit-Tenant Loans (CTLs)

Equipment Leases

Financial Institutions

Ground Leases

Insurance

Middle Market Lending

Project Finance

Real Estate, REITs

Specialty Finance

CRE Loans, Other

Funds:

Closed-end Funds

Credit Funds

CRE Funds

Direct Lending Funds

Feeder Funds

Infrastructure Funds

Liquidity Funds

Mezzanine Funds

Mixed Strategy Funds

Opportunistic Funds

Real Estate Funds

Structured Debt Funds

Click here to view sample Private Placement transactions.