Risk Commentary

Central Bankers' Dilemma (May 2023)

Central banks have always had massive power. Over the past 15 years, as they battled the 2008 Credit Crisis, they were endowed with even greater powers. Understanding the pressures facing the central banks and their potential behavior is critical for any sophisticated institutional investor.

Let’s Get Real

At the end of the day, the central banks’ primary job is to maintain economic order and facilitate the operation of their respective economies. Long gone are the days when each unit of currency was backed by precious metals. Hence, it is merely faith that maintains the system - faith that the central banks will do the right thing to keep the economies on track. In reality, most people and institutions have little choice as all developed countries are on the same path.

A test came following the 2008 Credit Crisis. Sovereign interest rates were suppressed to zero or below (via quantitative easing) and more recently, courtesy of Mr. Bernanke, helicopter money was used to stimulate demand.

Alas, all the stimulus, both monetary and fiscal, has left most developed nations with the twin problems of inflation and elevated debt (as measured by debt to GDP).

While recent efforts have been focused on fighting inflation, over time, elevated debt is likely to pose a more acute dilemma. Let’s focus on the most dire cases, even though these are not isolated instances.

In 2021, Italy had general government gross debt of $3.16 tn [1] and GDP of $2.11 tn [2]. With prevailing yields on Italian 10-year bonds at 4.3% [3], and 2022 deficits of $160bn [4], one could argue that the current levels are simply unsustainable. Perhaps the Italian national budget could be cut massively, but the reaction would likely be stronger than that in France over the two-year deferral of retirement benefits. French protests are likely to result in Macron’s defeat.

Thus, fiscal measures are unlikely to be palatable. Well, there is always the central bank of Europe, and a possible mutualization of debt. Yes, during COVID the Rubicon was crossed via the issuance of pan-EU debt, and before that with Mario Draghi’s purchasing of periphery country debt to reduce spreads.

Our view is that after Western governments determine that fiscal restraint is difficult and that purchases of sovereign debt by the central banks and commercial banks has limits, the next step might be a legerdemain via the issuance of Special Drawing Rights by the IMF. This action was undertaken previously in 2009 for $250bn [5] and 2021 for $650bn [6]. However, it is likely to only push the problem forward a few years. In the meantime, we expect there will be massive pressure to maintain interest rates at moderate levels to minimize pressure on federal budgets.

Some Humility

To paraphrase baseball great Yogi Berra, predictions are difficult especially when they concern the future. We have laid out what we believe are reasonable arguments, but much can change and very quickly. Times of stress can cause massive, unexpected shifts and therefore vigilance is paramount.

Commercial bank action offers a challenge for many institutional investors in the short run; a few quarters of underperformance runs the risk of a substantial drawdown in assets. Hence the herd mentality sets in such that the best stance, at least in the short run is to track the behavior of the crowd, which can typically be defined by indexes. Unfortunately, such an approach runs the risk of missing out on some of the best opportunities available.

Seth Klarman of Baupost, one of the three investors Warren Buffett the value investor identified as a person he would invest money with if he disbanded Berkshire Hathaway, stated that investing involved the intersection of financial analysis and psychology. The psychology part appears to be dominating currently as conditions are particularly attractive in private debt. Hence, our term the “Goldilocks Environment”.

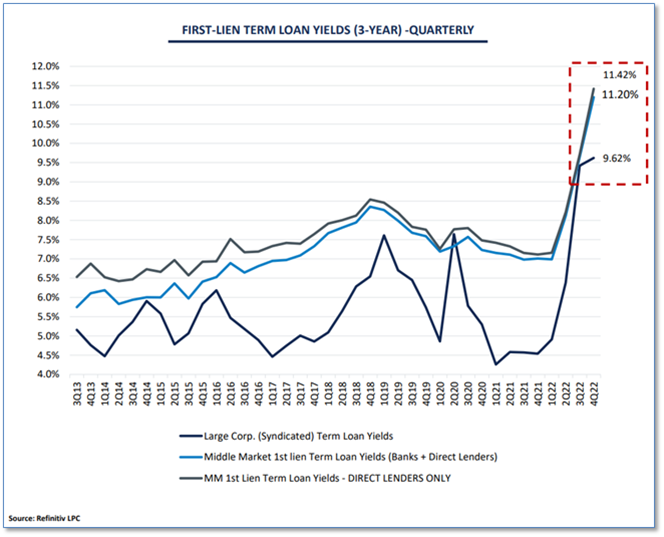

From a fixed income investment management perspective, the yield on both new and floating rate investments has risen due to the rise in treasury levels and to some extent spreads. The issue is whether estimated losses have risen in a manner to offset the increased yields. Early indications are that they have not and with the focus of many central banks on the overall market stability, we doubt that losses will rise to offset the benefits of increased yields. Hence, we consider the current environment as “Goldilocks” and it is likely to dissipate as the Fed moderates rate increases. The below chart suggests that yields have risen 450 bps or more over the past year.

Figure I: First-Lien Term Loan Yields (3-Year)- Quarterly

One of the major rating firms estimates that default rates will rise to 2.0%, and 4.25% in the pessimistic case.

"Among rated loan issuers, we expect the trailing-12-month Leveraged Loan Index default rate to more than double to 2.0% by June 2023 under our base case, still under the long-term historical average rate of 2.5%. Under our pessimistic case, we think defaults could increase to 4.25% over the same period." [7]

Given typical 50% recovery rates, the estimated loss in the most pessimistic case would approximate 2.125% (i.e., half of the 4.25%), which is more than covered by the yield. Hence, from an economic perspective, the returns appear to be attractive.

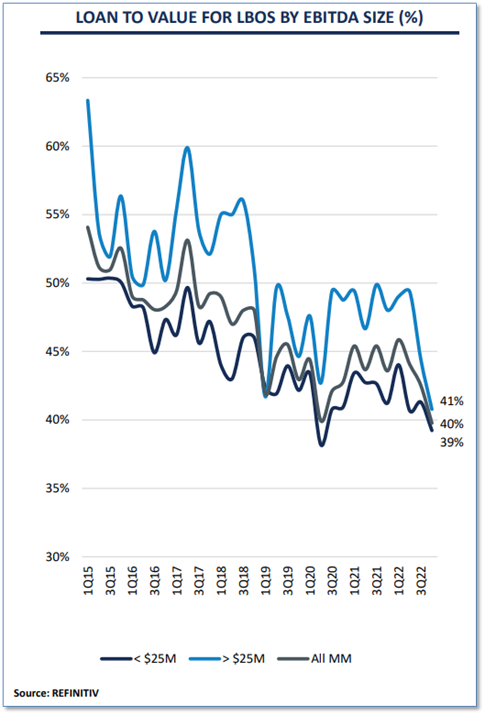

Before accepting the situation at face value, perhaps it is worthwhile reviewing the credit quality conditions. The below chart suggests that the loan to value for LBOs has declined over the past couple of years.

Figure II: LTV for LBOS by EBITDA Size

Perhaps it is worthwhile asking the question of why the current conditions exist and will they persist or become more attractive. Our view is that money flows are based on recent performance and that the rise in Fed funds rates and interest rates resulted in many investors reducing allocations. Thereby a mismatch was created. One could also argue that it is less an issue of reduced allocations than investors becoming more cautious. Concerning future conditions, see the next section.

The Inflation Witch

Regarding inflation and interest rates, we have been at these levels before, and the markets have thrived. The issue that has spooked the markets is the rapid rise in rates and the seeming persistence in inflation. However, Professor Steven Hanke of Johns Hopkins University has been fairly accurate in his inflation estimates, basing his predictions on the levels of M2 growth. Per a recent WSJ editorial High Inflation Will End Soon:

“We are lowering our forecast for the year-over-year inflation rate from 5% to between 2% and 5% at the end of 2023” [8]

As can be seen below, M2 has declined recently. Time will tell whether the “Inflation Witch” is dead.

Figure III: Real M2 Money Stock

Figure IV: Inflation & Unemployment

Ukraine Update

We cover Ukraine because of its massive impact on the global economy. To the angst of supporters on both sides of the conflict, it appears to be taking the usual turn which is that of a long-massive costs in terms of people, resources, and disruption. Gains for Putin appear elusive as do the gains for the West. As usual, the winners are the defense-related firms and eventually, those involved in the reconstruction efforts. The European Union escaped the brunt of restricted natural gas supplies courtesy of a warmer than expected winter and a scramble for alternative sources. The concern is that Western support will wane, and that Ukraine will have difficulty offsetting Russia’s massive personnel advantage. So far, Ukraine has held its own. A game-changer would be Ukraine’s retaking Crimea, which might prompt armistice discussions.

Commodity Super Cycle

Commodity Super Cycles are caused by a dramatic rise in demand or cut in supplies. The last major one from our perspective was the cutting of petroleum supplies via the oil embargo prompting a significant rise in gasoline prices. Despite much talk of a shift to wind and solar power, the reality is that much of the world remains dependent on fossil fuels. Moreover, the push for electric vehicles has created demand for a variety of minerals. The problem is that for many institutional investors including banks, mining does not meet ESG standers resulting in restricted capital investment. Coal and petroleum production need to be watched.

____________________________________________

[1] https://fred.stlouisfed.org/series/GGGDTAITA188N

[2] https://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=IT

[3] https://www.wsj.com/market-data/quotes/bond/BX/TMBMKIT-10Y

[4] https://www.worlddata.info/europe/italy/debt.php

[5] https://www.imf.org/external/np/exr/cs/news/2009/cso79.htm

[6] fzhttps://www.imf.org/en/Topics/special-drawing-right/2021-SDR-Allocation

[7] https://www.spglobal.com/_assets/documents/ratings/research/101567579.pdf

[8] Feb. 15, 2023, WSJ

How we can help

Founded in 1995, Egan-Jones is a Nationally Recognized Statistical Rating Organization (NRSRO) and is recognized by the NAIC and is certified by ESMA. We can help in the following areas:

Requested Ratings – we assist investors access private and public markets via ratings.

Subscription Ratings – we provide early, accurate, and independent credit rating research.

Independent Proxy Research and Recommendation/Voting – we assist fiduciaries fulfill their voting and record-keeping obligations.

Egan-Jones rates a wide variety of private placements:

Aircraft Lease and Loans

Airline Lease Back

Asset-backed loans

Bank, BDCs

Credit Facility/ Warehouses

Corporates

Credit-Tenant Loans (CTLs)

Equipment Leases

Financial Institutions

Ground Leases

Insurance

Middle Market Lending

Project Finance

Real Estate, REITs

Specialty Finance

CRE Loans, Other

Funds:

Closed-end Funds

Credit Funds

CRE Funds

Direct Lending Funds

Feeder Funds

Infrastructure Funds

Liquidity Funds

Mezzanine Funds

Mixed Strategy Funds

Opportunistic Funds

Real Estate Funds

Structured Debt Funds

Click here to view sample Private Placement transactions.