Overview

Typically, tightening credit spreads are an indication that the market believes the risk of defaults is declining, and therefore, a greater portion of the stated yield will be realized. An alternative view is that there is excess liquidity in the market, and investors need to put cash somewhere. In this installment, we address both possibilities and hopefully provide some benchmarks for sophisticated institutional investors and risk managers.

Where we are

The threat of increased defaults has been mentioned monthly over the past 5 years, starting with the COVID crisis, the ramp-up in interest rates, the SVB collapse, the election of two new administrations, the invasion of Ukraine, and, more recently, the introduction of tariffs. Like the Energizer Bunny, the market keeps making progress, with most indices recently reaching all-time highs.

On the fixed income side, spreads have likewise shown strong resilience, as indicated by the chart at the top of this installment. While this action is comforting to many, the issue is whether the probability of future defaults is declining.

The Black-Scholes model, which considers equity values and equity value volatility, indicates that equity markets are strong. On both fronts, there is a degree of solace (to quote one of our favorite Bond movies). Not only are indices at strong levels, but volatility, as measured by the VIX, is also at moderate levels:

Some Refinement; Our Crowd

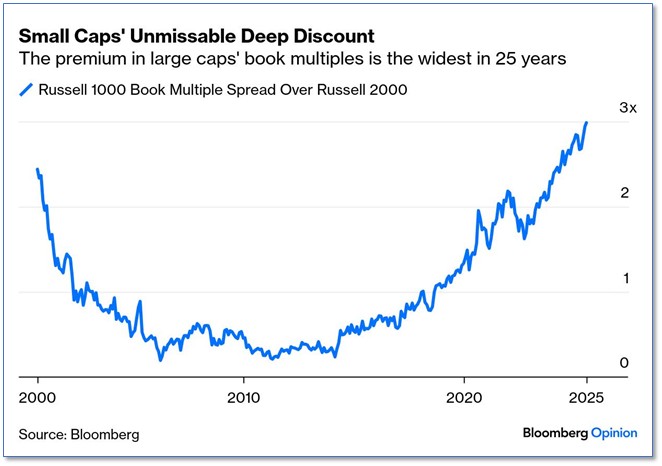

While the above commentary is comforting, the reality is that the equity markets are now dominated by the tech/AI crowd (e.g., Nvidia, Meta, Alphabet, Oracle, etc.) who are far removed from the typical players in the fixed income crowd. Supporting this notion is the graph below, which shows that, for the typical middle market firm, the valuation multiples are at recent lows. So where does that leave us?

Where We Are Going; Skating to Where the Puck Is Going

Our view is that, while we always worry about a collapse, short of a significant war (e.g., between China and Taiwan), there appears to be little that might catalyze a major run. Yes, there will continue to be concerns, particularly with the current administration’s record pace of changes, but it appears that some of the major issues might be addressed. Furthermore, as stated in prior installments, the Fed and other central banks stand ready to address the most significant market problems.

Our Approach

Since our founding in 1995, we have prided ourselves on being able to predict failures before they became apparent to most market participants. See future installments chronicling our calls on Enron, WorldCom, GE, GM, Bear Stearns, Amazon, and others.

A reasonable measure for private debt ratings performance is the discrepancy between the expected defaults and the actual defaults. For example, if an investor held 10 single “B” rated diversified instruments, and the one-year probability of default was 10% for each, then after one year, the expected defaults would be 1. If more than 1 default occurred, it would be reasonable to conclude that the ratings were too generous.

We performed the same math on all private debt ratings and found that far fewer defaults occurred than expected. Regarding defaults, there will always be some; the core issue is whether the actual defaults materially exceed expected defaults.

Conclusion

While continued vigilance is a prerequisite for investment success, there is no obvious cause for above-average concern presently.